Wash trading is known to be common in incipient financial markets, and decentralized finance (DeFi) is no exception. Solidus Trade Surveillance data shows that since September 2020, liquidity providers (LPs) on Ethereum-based decentralized exchanges (DEXs) have wash-traded at least $2 billion worth of cryptocurrency, manipulating the prices and volumes of more than 20,000 tokens. In aggregate, LPs have executed wash trades in 67% of the almost 30,000 DEX liquidity pools in our sample, and wash trading has constituted 13% of the these pools' total trading volumes.

The liquidity pools we studied comprise just 1% of all pools by count and 0.3% of all pools by volume across every blockchain and DEX. As such, this is a lower bound estimate; the true amount of DEX-based wash trading that has taken place since September 2020 is likely an order of magnitude larger.

What is wash trading, and why does it happen in crypto?

Wash trading is a form of market manipulation in which one entity simultaneously buys and sells the same asset, creating a false impression of market activity despite the trade reflecting no change in beneficial ownership. In crypto, liquidity is fragmented across a variety of centralized and decentralized venues, resulting in smaller markets that are easier to manipulate. A number of entities are therefore known to execute wash trades:

Exchange and marketplace operators: To report higher trading volumes to data aggregators, potential investors and prospective users

Crypto market makers: To hit the order-to-trade ratio requirements set forth in their contracts with centralized exchanges & token issuers, or to anchor a token’s market price above the strike price of a call option they may have negotiated with that token’s issuer

Individual speculators: To top the leaderboards that crypto exchanges and NFT marketplaces create to reward their most active users through token airdrops

Token deployers: To trick traders into investing in rug pulls, qualify for listings on centralized exchanges, and/or mislead investors about their project’s health

While centralized exchanges and market makers typically have the option to wash trade at a no cost or a lower cost on centralized venues where orders are matched and executed off-chain, token deployers – especially scam token deployers – have some of the strongest incentives to wash trade on decentralized venues that execute trades on-chain, where transaction fees are higher. This is because, as we illustrated in part one of our Crypto Market Manipulation Report, DEX liquidity pools are often their token’s first listing venue. This means that a token deployer’s ability to either get their token listed on a centralized exchange or rug-pull their investors for profit depends upon their skill in attracting speculators to the liquidity pool on which their token is traded. We find that many token deployers will resort to DEX-based wash trading to do so.

How does DEX-based wash trading work?

DEX-based wash trading can be divided into two main typologies:

A-A wash trading

Multi-party wash trading

DEX-based A-A wash trading

In A-A wash trading, a single cryptocurrency address (“0x1”) sits on both sides of the token swap. This means that 0x1 acts as both (a) the dominant liquidity provider in the pool and (b) the “swapper” exchanging token one for token two (or vice versa). Whenever these trades occur, no change in beneficial ownership takes place – and yet each swap manipulates the less-established token’s price and volume, creating an artificial market signal.

We have identified $960 million worth of A-A wash trades since September 2020 in our sample of DEX liquidity pools.

DEX-based multi-party wash trading

In multi-party wash trading, the addresses of the liquidity provider(s) and the swapper(s) are different, but the addresses are controlled by the same entity. For example, 0x1 may act as the pool’s dominant liquidity provider while 0x2, 0x3 and 0x4 pretend to be distinct swappers, trading token one for token two (or vice versa) to drive up token two’s trading volume. This method is likely preferred by entities seeking to avoid detection and inflate the number of investors that appear to be buying or selling the token.

We have identified approximately $1.1 billion worth of multi-party wash trades since September 2020 in our sample of DEX liquidity pools.

Case Study: SHIBAFARM

In mid-May of 2021, a token named SHIBAFARM came online, and its price began a continuous, precipitous climb. It had no website, roadmap, or public offering to credit for the rally; instead, its creator relied on investor FOMO about a similar memecoin’s rapid rise. The week before, Shiba Inu (SHIB) had skyrocketed 2,500% almost overnight.

SHIB to USD, 5/6/21-5/10/21

Source: CoinMarketCap

SHIBAFARM’s deployer used two technical tricks to create the impression that SHIBAFARM was SHIB’s second coming. The first was a honeypot: a type of rug pull in which a token’s smart contract is programmed to block the token’s buyers from subsequently selling. This meant that SHIBAFARM faced no sell pressure — no matter how hard investors tried.

The second was a “chained” multi-party wash trading strategy. After deploying SHIBAFARM, its creator (address 0x9e8, bottom-center in the below chart) began transferring large sums of 80-400 Ether (ETH) to a set of newly created wallets. These wallets would then execute 5-20 ETH buys of SHIBAFARM against the liquidity 0x9e8 provided – resulting in no change in beneficial ownership – and transfer the remainder to another fresh wallet.

This wallet would, like the one before it, swap some ETH for SHIBAFARM and then pass the remaining ETH on to a new address. 0x9e8 repeated this process more than 30 times to manufacture rapid, organic-seeming growth in SHIBAFARM’s volume and price. In aggregate, SHIBAFARM’s deployer & liquidity provider 0x9e8 acted as though they were 25 distinct traders, and their 30+ swaps constituted more than 40% of SHIBAFARM’s volume.

Using these two deceptive techniques, 0x9e8 engineered a hockey-stick price chart for SHIBAFARM. This chart – which we’ve recreated below to include liquidity withdrawals (in red) and a distinction between organic buys (in light green) and inorganic buys (in light gray) that decentralized market data providers do not – appears to have tricked more than 50 other traders into investing in SHIBAFARM.

The result: in the span of two hours on May 15th, 2021, 0x9e8 made off with profits of approximately $2 million — all without “selling” SHIBAFARM once. As the sole liquidity provider in the pool that paired their scam token with ETH, 0x9e8 was the main counterparty in every one of the other traders’ ETH-to-SHIBAFARM swaps. To take profit, 0x9e8 simply had to withdraw two-sided liquidity from the pool, which now consisted of much more ETH (worth about $3,700 at the time) and less SHIBAFARM (effectively worthless) than before.

Two nights later, SHIBAFARM’s deployer created a new token, SHIBASWAP, and repeated this process from scratch. Since 2021, SHIBAFARM’s deployer has made and manipulated the prices of more than 50 scam tokens.

Wash trading prevention and detection: A proven path to fairer markets

In DeFi, a regulatory question remains regarding who is responsible for wash trading prevention and detection. However, there is no question that fairer markets are essential for sustainable growth. As we've demonstrated in this report, DEX-based wash trading is detectable — and in many cases even preventable. In traditional finance, self-trade prevention functionality (STPF) is built into modern exchanges. Applied to DEXs, such functionality could prevent the millions of A-A-type wash trades we detected. Multi-party wash trading is similarly addressable. By tracing token flows between wallets providing liquidity and trading in the same pool, exchanges and regulators can identify suspicious clusters of wallets for further investigation.

Wash trading may be a new problem for DEXs, but, much like insider trading, it’s one with a proven solution.

Methodology

We focused our analysis on Ethereum-based DEXs that leverage constant product market maker (CPMM) models and that do not support concentrated or one-sided liquidity provision – although the threat of wash trading on such DEXs is also present, but with different mechanics. Within this DEX subset, we further narrowed our sample to include only the liquidity pools of those DEXs that met the following additional criteria:

The pool’s first liquidity provider provided the vast majority of liquidity – more than 90% of both token one and two – at all times during trading

the ratio of trades relative to traders that swapped tokens using the pool was greater than or equal to two

All notional U.S. dollar amounts were calculated using the average daily ETH-USD price at the open from September 1st, 2020 to August 31st, 2023 — $2,028.

Trusted by compliance teams and regulators globally

Built for Data Complexity

Normalizes non-standard feeds and on/off-ramp data into one real-time schema, while crypto-native models cut through volatility to flag wash trades, spoofing, and insider flow, even amid extreme price swings or cross-venue price gaps.

Future-Proofed for Evolving Crypto-Specific Schemes

Monitors manipulation across both on- and offchain, from insider trading on DEXs, cross-venue schemes spanning spot/derivatives or CeFi/DeFi to native onchain threats throughout the asset life cycle.

Real-Time Intervention Before Risk Escalates

Real-time alerting surfaces risk instantly, enabling timely intervention in a global, 24/7 “always-on” market and instant settlement that legacy batch processing can’t offer

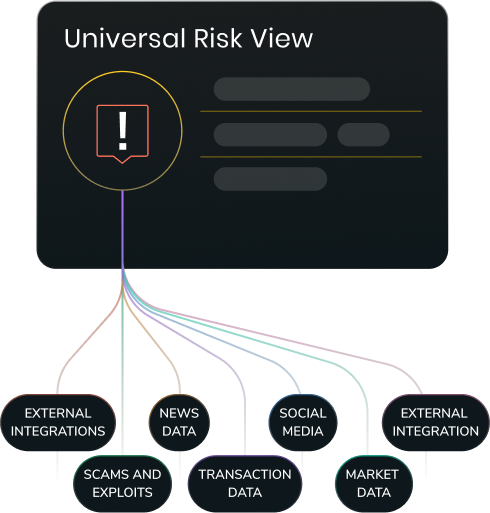

See Risk Across Trades, Transactions & KYC

Unifies trades, transactions, KYC, and behavioral signals in one view—uncovering risks siloed systems miss like account takeovers, new-account scams, and transactions that appear legitimate in isolation but raise suspicion when analyzed against broader trading behavior.

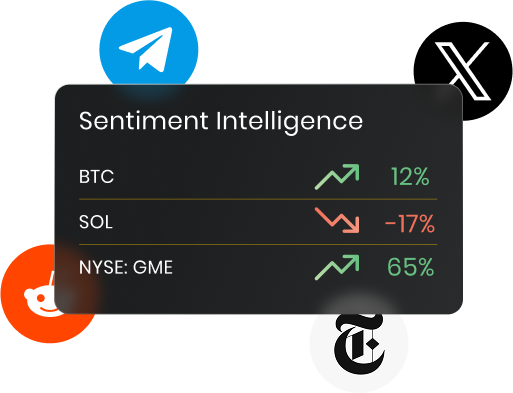

Crowd-Driven Crypto Sentiment Intelligence

Machine-learning sentiment analysis distills signals from messy, unstructured data across Reddit, X, Telegram, and news sources – flagging symbol-level sentiment shifts in real time.

Venue-Agnostic Data Architecture

Venue-agnostic approach to market data delivers high speed and scalability across all digital and traditional asset classes, with fallback mechanisms for uninterrupted surveillance even without full order-book depth.